8 Lease-To-Own Programs

Why you should?

Home Prices are soaring. Already in the Greater Metro Atlanta area, median home prices have increased from an average of $315,000 in 2020 to $400,000 in 2021, and $438,500 in 2022. When you lease to own, you lock in your home price, so when the home appreciates in value in the coming years, you will be able to lock in your purchase price now.

Who do we typically help?

Important Factors to Consider:

How Does Lease To Own Work?

Step 1: Complete the application to qualify. You can apply to each program available with no impact to your credit.

Step 2: Once you’re approved, you’ll receive a budget to go home shopping. As your Realtor, we will come up with a list of your needs and wants and tour properties that are available in your desired areas.

Step 3: The company pays for the home in cash and you would submit a down payment in the amount of 1-3.5% of the purchase price of the home. Or with Home Partners your down payment would be two months rent. Each program has their own down payment requirements. This down payment will later be used towards the purchase of the home when you get ready to qualify for a mortgage loan.

How do you qualify?

Each program has its own income verification process. The acronym that Elegance Realty uses to simplify these requirements is "CSI".

C = Credit

S = Savings

I = (Household) Income

Documents

Here are some of the documents you may potentially need when applying.

Home Prices are soaring. Already in the Greater Metro Atlanta area, median home prices have increased from an average of $315,000 in 2020 to $400,000 in 2021, and $438,500 in 2022. When you lease to own, you lock in your home price, so when the home appreciates in value in the coming years, you will be able to lock in your purchase price now.

Who do we typically help?

- Clients that cannot currently qualify for a mortgage

- Last minute problems closing with a mortgage

- Bridge between renting & purchasing

Important Factors to Consider:

- Residents only commit to a one-year lease term. You have the ability to renew your lease in one-year increments, for up to 3 to 5 years. Before signing your lease, you are given your monthly rent and agreed purchase price for the following years.

- These programs do not provide mortgage financing nor guarantee that clients will obtain a mortgage at the end of their lease.

- You are encouraged to apply for more than one program; however, you want to choose the best program that meets your needs and budget. Therefore, carefully review the qualification requirements of each program below and on the application links below prior to applying. Should you need assistance choosing the programs to apply for, your Elegance Realty Buyer's Specialist can recommend you to the appropriate programs to apply for.

How Does Lease To Own Work?

Step 1: Complete the application to qualify. You can apply to each program available with no impact to your credit.

Step 2: Once you’re approved, you’ll receive a budget to go home shopping. As your Realtor, we will come up with a list of your needs and wants and tour properties that are available in your desired areas.

Step 3: The company pays for the home in cash and you would submit a down payment in the amount of 1-3.5% of the purchase price of the home. Or with Home Partners your down payment would be two months rent. Each program has their own down payment requirements. This down payment will later be used towards the purchase of the home when you get ready to qualify for a mortgage loan.

How do you qualify?

Each program has its own income verification process. The acronym that Elegance Realty uses to simplify these requirements is "CSI".

C = Credit

S = Savings

I = (Household) Income

Documents

Here are some of the documents you may potentially need when applying.

- Savings: Bank Statements, 401K, Gift Letter

- Income:

- Hourly/Salary: Recent Pay Stubs

- Independent Contractors: Recent Pay Stubs

- Self Employed: Bank Statements, Tax Returns, Profit and Loss Statement

Divvy

Rent your dream home while Divvy helps you save for a down payment. You can buy the home from us whenever you’re ready, or walk away and cash out your savings.

QUALIFICATIONS:

|

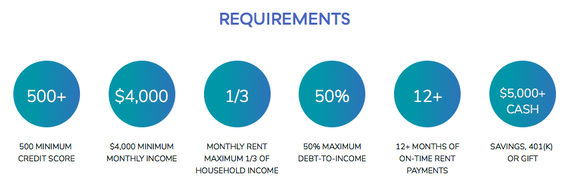

Dream America

Rent your dream home while Dream America helps you save for a down payment. You can buy the home from us whenever you’re ready, or walk away and cash out your savings.

QUALIFICATIONS:

12-Month lease-to-own

Watch intro video/client testimonials: Click Here to learn about the Dream America program! Click Here to listen to Trina who is now a homeowner! Click Here to hear Denita discuss how Dream America is helping Veterans! |

Halo |

Home Partners of America |

QUALIFICATIONS:

Based on standard FHA down payment guidelines, we require that you have cash equal to 3.5% of the purchase price in order to enter the HALO program. Lease terms are determined on an individual basis and factor in the cost of the home, property taxes, HOA fees (if any) and insurance costs. Rents start at $1,300/month. |

QUALIFICATIONS:

Several factors taken into consideration: (household income, rent-to-income and debt-to-income ratios, rental and housing history, employment history, criminal history, and FICO® scores.) When there are multiple people, not an average of the scores. Will also look at the income. Whoever has the highest income, their credit score will carry the heaviest weight. Will outline the maximum Monthly Rent of the home for which the prospective resident qualifies. Each year, a resident's Monthly Rent increases by no more than 3.75% over the previous year’s Monthly Rent. For example, if the Monthly Rent for Year 1 is $1,400 per month, the increase for the next year is $50/month (i.e., $1,400 x 1.0375)*. |

Landis

Landis makes it easier to buy your new home. They will provide you with an easy and transparent process to transition seamlessly from renting to owning. They have been funded by celebrities such as Jay Z and Will Smith in an effort to help more people own and build wealth with their homes instead of renting.

QUALIFICATIONS:

|

Pathway Homes

Pathway is an amazing program that allows you to rent your home now and buy it later. Requires you to rent for at least one year before you can purchase the home with a mortgage.

QUALIFICATIONS:

|

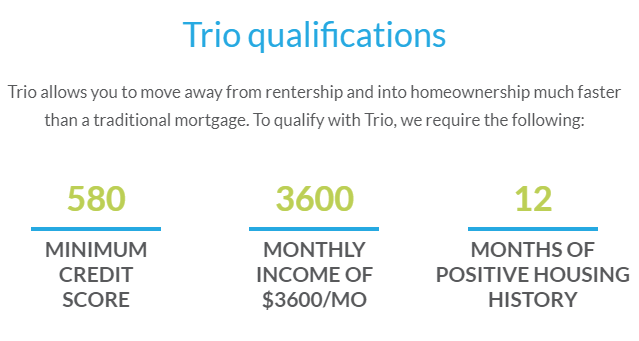

Trio

To complete your application, you will need to provide details of your income and savings. You will also need to provide contact information for your employer and landlord. If including a co-applicant, make sure they are available to provide their details as well. All applicants should be present to complete the application as accurately as possible.

A reminder of our minimums:

|

|

The following program only provides a 6 month lease, therefore you must already have a Preapproval Letter from a Mortgage Lender in order to qualify for this program.

Ribbon Home

|

Ribbon Buy

Price range: 150K - 700K 4 acres and under Built after 1975 or renovated NO: mobile, manufactured, modular, seller possession, as-is, flips, Fixer-uppers, Renovation Specials, investment/vacation/secondary homes, foreclosures, short sales, estate sales (by case), seller post-occupancy. |

The steps in the Ribbon program are:

- Step 1: Client must have a Preapproval Letter from a Mortgage Lender

- Step 2: Client must accept the Ribbon Program Agreement to be ready to make an offer!

- Step 3: Your Agent adds properties to Client's Ribbon Profile.

- Step 4: Ribbon's team of experts works on valuing the properties to determine their maximum purchase price. They strive to provide you with the most competitive and accurate price possible.

(Valuations typically take less than 24 hours to complete. - Step 5: Ribbon buys and reserves your new home

- Step 6: The Ribbon fee is due when we buy the home (typically paid by the seller)

- Step 7: Client rents their new home from Ribbon while you secure financing

- Step 8: Once Client is ready to repurchase their home, they buy it back from Ribbon at the same price

© 2006 - 2023 Elegance Realty, LLC

All rights reserved.

Office: 678-757-5364 | [email protected]

Elegance Realty provides Professional Real Estate Services to Buyers and Sellers in the Atlanta GA metropolitan area.

All rights reserved.

Office: 678-757-5364 | [email protected]

Elegance Realty provides Professional Real Estate Services to Buyers and Sellers in the Atlanta GA metropolitan area.